Overview

Overview |

Uninsured motorist (UM) and underinsured motorist (UIM) are first-party coverages, meaning that the payout is for the insured drivers on the policy, NOT the third party. Often just called uninsured motorist, this coverage refers to two separate insurance coverages that are typically categorized together:

- Uninsured motorist bodily injury and property damage: available for damages caused by an at-fault driver who doesn't have any insurance

- Depending on the state, this could also apply to a hit-and-run driver where the owner cannot be identified

- Underinsured motorist bodily injury and property damage: available for damages caused by an at-fault driver who doesn't have enough liability coverage to cover all of the damages from the accident

The limits of UM/UIM coverage are broken up into bodily injury and property damage, similar to liability. UM/UIM is not a required coverage in all of our states. Here are the requirements by state for UM/UIM bodily injury and property damage:

| UM/UIM Bodily Injury | ||||||||

|---|---|---|---|---|---|---|---|---|

| IL | IN | MD | OH | TN | TX | VA | GA | |

| Required? | Y | N | Y | N | N | N | Y | N |

| Minimum limit per person/accident | $25,000/ $50,000 | $50,000/ $50,000 | $30,000/ $60,000 | $25,000/ $50,000 | $25,000/ $50,000 | $30,000/ $60,000 | $50,000/ $100,000 | $25,000/ $50,000 |

| UM/UIM Property Damage | ||||||||

|---|---|---|---|---|---|---|---|---|

| IL | IN | MD | OH | TN | TX | VA | GA | |

| Required? | Y | N | Y | N | N | N | Y | N |

| Minimum limit | $15,000 | $25,000 | $15,000 | $7,500 | $15,000 | $25,000 | $25,000 | $30,000 |

| Deductible | $250 | $0 or $300 | $250 | $250 | $200 | $250 | $200 | $250, $500, or $1000. |

UM/UIM Bodily Injury & Property Damage

UM/UIM Bodily Injury & Property Damage |

UM/UIM bodily injury covers you, the insured members of your household, and your passengers for medical expenses, loss of income, funeral expenses, pain, and inconvenience that are caused by an uninsured or underinsured vehicle, up to your policy limits.

The amount payable under underinsured bodily injury will be reduced by the total amount paid towards bodily injury by the responsible party. Generally, you cannot get more than your limits no matter who is paying for the damage.

UM/UIM property damage covers your insured vehicle for property damage caused by an uninsured or underinsured vehicle, up to your policy limits. The payout of underinsured property damage works similarly to bodily injury in that the available limit will be reduced by the total amount paid towards property damage by the responsible party.

UIM BI Payout Example

You're a Virginia policyholder with $50,000/$100,000 limits for UIM BI. A driver carrying state minimum limits hits your car and causes you $55,000 of bodily injury.

Their insurance pays up to the limit of $30,000, leaving you with $25,000 of bodily injury costs. Your per-person limit of $50,000 is reduced by the $30,000 already paid towards bodily injury, so you're left with $20,000 of UIM BI that can be used.

UM Property Damage in IL and OH

For UM property damage in Illinois and Ohio, the owner or operator of the uninsured vehicle involved must be identified by either their name and address, registration number and description of the vehicle, or any other information that will prove there is no applicable property damage insurance. You can’t carry both UMPD and collision in either state.

UM Property Damage in IN

Similar to IL, for UM property damage in Indiana, the owner or operator of the uninsured vehicle involved must be identified by either their name and address, registration number and description of the vehicle, or any other information that will prove there is no applicable property damage insurance. The deductible for UMPD in IN can be selected at either $0 or $300.

UM Property Damage in GA

Elephant’s lowest liability limits are slightly different than the state minimums. This was a deliberate choice to make filing easier to maintain. We will have to be careful with our word choice!

We CANNOT say that we offer the “state minimum.”

We CAN say:

- “I’ve set you up with our lowest limits.”

- “I’ve got you set up with our/Elephant’s minimums for liability.”

If asked..."Are these coverages the state minimums?"

- Elephant decided to set our minimum property damage at $30,000 to give our customers a little extra cushion.

- With the average cost of cars getting more expensive every year, we like to start our customers with $30,000 of PD instead of the state minimum of $25,000.

If asked..."Does that cost more?"

- Since we don’t actually offer a rate for lower property damage, and I wouldn’t have information on other companies, I wouldn’t be able to speak to that.

Waiver Requirements

Waiver Requirements |

Depending on whether the customer elects to waive or carry UM/UIM at a lower limit than liability, there are different waiver requirements for each state. Once a policy is bound, the customer has 7 days to sign and return the waiver, or the coverage will be added back on the policy. Here are the waiver requirements by state:

| IL | IN | MD | OH | TN | TX | VA | GA | |

| No UM/UIM | N/A* | waiver | N/A** | N/A | waiver | waiver | N/A** | waiver |

| UM/UIM with lower limits | N/A* | waiver | waiver | N/A | waiver | N/A | waiver | waiver |

* IL requires UMBI at state minimum limits. UMPD can be left off without a waiver.

** VA and MD require UMBI and UMPD

See more about waivers HERE.

EUIM (MD)

EUIM (MD) |

In addition to UIM in MD, there is an enhanced underinsured motorist coverage that customers can elect to carry. Here is a breakdown of the differences between typical underinsured motorist and enhanced underinsured motorist (EUIM).

Generally, with typical UIM, your payout will never be larger than your limits no matter who is paying for the damage - whether that's your insurance or another party.

With enhanced underinsured motorist, the amount of coverage you have access to isn't affected by other payouts. Even when carrying the same limits as the third party, you would still have access to your full UIM limits in the event of an accident. The coverage essentially makes your underinsured payout work independently of any other party's payments towards damages. Keep in mind that the total payout will never be more than the actual damages suffered.

EUIM Waivers

Depending on the customer's UM/EUIM selection, there may be a waiver. Here are the three options that the customer has regarding UM/EUIM:

The customer has 7 days to sign and return the waiver. If the waiver is not signed, the coverage will default to NO EUIM and matching limits. View more on waivers here.

The customer has 7 days to sign and return the waiver. If the waiver is not signed, the coverage will default to NO EUIM and matching limits. View more on waivers here.

With option 1, you must advise your customer before bind that EUIM is not included on the policy and that it can be added at any time for an additional premium:

I did not include EUIM which is available for an extra charge.

How EUIM Works

With standard UIM

You are involved in an accident where the other driver doesn't have enough insurance. $17,500 worth of property damage is done to your vehicle. The at-fault driver can only pay you $5000 towards the damages. To meet your $15,000 property damage limit, Elephant will only pay another $10,000. This leaves you having to come up with $2,500 to take care of the rest of the damage.

Example with EUIM

Looking at the same accident, only this time you carry EUIM. When the other party pays you $5000, it goes in a separate "bucket" and doesn't affect your $15,000 limit. Elephant still has your full limit to work with and will pay out $12,500 to make up the rest of the property damage. In this example, you owe nothing additional out of pocket (deductibles will apply).

Explaining EUIM to a Customer

You can wait until coverage counseling before bind to let your customer know about EUIM. If they have questions about what it is, you could use the suggested scripting below.

- If someone causes a lot of damage and their insurance can only cover part of it, your normal underinsured motorist could kick in.

- However, you would never receive a payout larger than your limits no matter where it comes from – your own company or the other person’s company.

- EUIM makes sure that the amount of coverage you have access to isn’t affected by other payouts.

- You have coverage if the person at fault has no insurance.

- However, if someone causes a lot of damage and their insurance can only cover part of it, your normal underinsured motorist could help cover the difference. So, for an additional premium, EUIM makes sure that the amount of coverage you have access to isn’t affected by other payouts.

- If you're worried about having enough coverage, I would recommend raising your overall limits. That may be a better option and give you the most helpful coverage.

- If someone causes a lot of damage and their insurance can only cover part of it, your normal underinsured motorist could kick in.

- However, with normal underinsured motorist, you would never receive a payout larger than your limits no matter where it comes from – your own company or the other person’s company. So, for an additional premium, EUIM makes sure that the amount of coverage you have access to isn’t affected by other payouts.

- If you're worried about having enough coverage, I would recommend raising your overall limits. That may be a better option and give you the most helpful coverage.

Added-On UM (GA)

Added-ON UM (GA) |

There are 3 options for UM in Georgia.

Georgia’s default is Added-On UM; if they choose to have it NO waiver is generated.

A WAIVER generates if…

- Choosing NOT to carry UM at all

- Electing to carry “Reduced” UM

- Carrying lower limits than Liability

What's the difference?

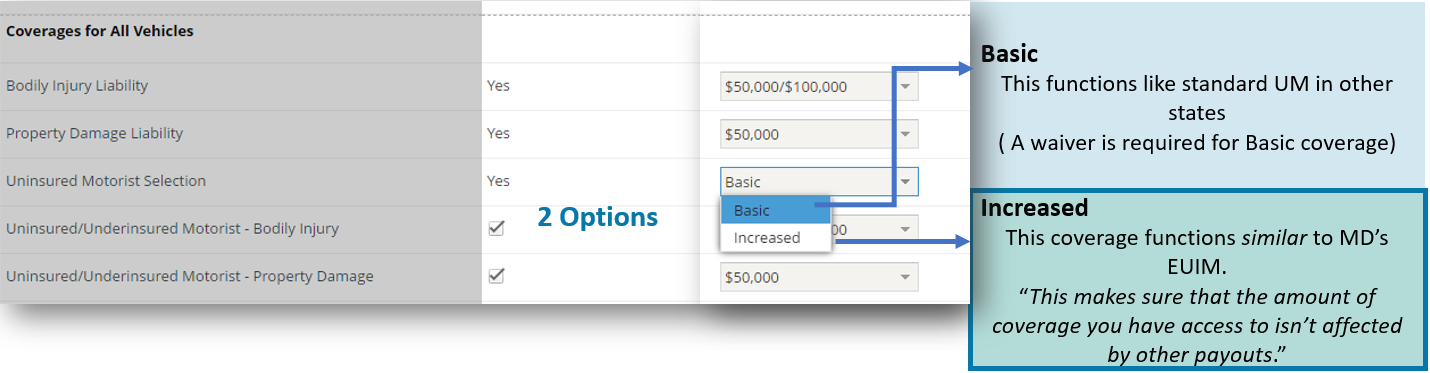

Increased Uninsured Motorist VA

Increased Uninsured Motorist VA |

There are 2 options for UM in Virginia starting for policies or renewals on or after 7/1/2023

Virginia's default will be Increased UM; if they choose to have it, NO waiver is Generated.

A waiver will be required if they want to keep Basic UM. This must be returned within 7 days of new business.

What's the difference?

Waivers by State

Waivers by State |

Some states require written proof that the customer rejected a coverage.

When this happens we send a waiver that can only be signed by the Named Insured.

Authorized users and Spouses cannot sign waivers

When binding an auto policy with waivers, it's very important to advise the customer that:

1) They need to sign and return the waiver within 7 days of binding the policy.

2) What happens when they don't sign the waiver within that timeframe

GA | IL | IN | MD | OH | TN | TX | VA | ||

Personal Injury Protection | - | - | - | if Guest only | - | - | if rejecting PIP | - | |

UM | Rejecting all UM | waiver | UMBI required | waiver

| UM required

| none | waiver

| waiver

| UM required |

| Lower limits than liability | waiver

| waiver | waiver | waiver

| none | waiver | none | waiver | |

Reduced UM | waiver | - | - | - | - | - | - | - | |

Added on UM | none | - | - | - | - | - | - | - | |

EUIM | - | - | - | waiver

| - | - | - | - | |

nothing

GA: Added-On Underinsured Motorist

In Georgia, there is an Added-On Underinsured Motorist coverage. If they do not want to have Added-On Um, customers have the option to carry:

- Reduced UM (which functions like standard UM in other states)

- Waive all UM from their policy

Both of these options require a waiver to be returned within 7 days, or their policy reverts to Added-On, and their price increases.

MD: Enhanced Uninsured Motorist

In Maryland there is Enhanced Underinsured Motorist (EUIM) coverage. We have to tell our customers that we didn't select this option, there is no waiver associated with not carrying the coverage.

In fact, if a customer wants to carry the coverage, then they must sign and return a waiver within 7 days. If they do not, then the coverage is removed.

Default Coverage if Waivers are not signed

Default Coverage if Waivers are not signed |

| Defaulted Coverage if Waivers are not signed | ||||||||

| STATE | GA | IL | IN | MD | OH | TN | TX | VA |

| PIP | - | - | - | Guest PIP | - | - | Included if not waived | - |

| Rejecting all UM | Included if not waived | UMPD included if not waived, UMBI Is required | Included if not waived | UM Required | N/A | Included if not waived | Included if not waived | UM Required |

| Lower Limits than Liability | Adjusted to same limits as liability | Adjusted to same limits as liability | Adjusted to same limits as liability | Adjusted to same limits as liability | N/A | Adjusted to same limits as liability | N/A | Adjusted to same limits as liability |

| Reduced UM | Will change back to added on if waiver is not signed | - | - | - | - | - | - | - |

| Added on UM | Default if waiver not signed | - | - | - | - | - | - | - |

| EUIM | - | - | - | Policy effective before 07/01/2024: Removed if waiver is not signed Policy effective on or after 07/01/2024: Added if waiver is not signed | - | - | - | - |

| UMP Deductible | $500 | $250 | $0 | $250 | $250 | $200 | $250 | $200 |

| Basic UM | - | - | - | - | - | - | - | Increased UM will be added on |

Waiving all UM (GA, IN, IL, TX, and TN)

UM will be added to their coverages if the waiver is not signed.

Electing lower UM limits than Liability (GA, IN, TN, MD, IL, and VA)

UM will be amended to match the limits of liability if the waiver is not signed.

Rejecting PIP (TX)

PIP will be added to their coverages if the waiver is not signed.

Electing to carry Guest PIP Only (MD)

Full PIP will be added to their coverages if the waiver is not signed.

Electing to carry EUIM (MD)

EUIM will be removed if the waiver is not signed.

Rejecting Added-on UM (GA)

Added on Uninsured Motorist will be added to their coverages if the waiver is not signed.

Note: Whether you are selecting reduced UM (similar to standard UM in our other states) or rejecting UM outright, they will need to sign a waiver.

Waiver Walkthroughs

Waiver Walkthroughs |

For all required waivers, only the customer will receive the email for the DocuSign, and they must be returned within 7 days.

PIP

GA: Added on UM

PIP, Med Pay, & Income Loss

PIP, Med Pay, & Income Loss |

Personal injury protection and medical payments are first-party coverages that pay for reasonable and necessary medical expenses and funeral services resulting from a motor vehicle accident. Medical expenses include services provided by a licensed health care provider such as ambulance, hospital, surgical, medical, dental, x-ray, professional nursing, and pharmaceutical services. To determine if the medical expense is reasonable and necessary, we may use independent sources such as physician exams, review of medical records, and programs for analysis of medical treatment and expenses. Medical payments coverage is called medical expense benefits in VA.

Here is a breakdown of first-party medical coverage offered by state, along with the statute of limitations, and whether income loss is included:

| GA | IL | IN | MD | OH | TN | TX | VA | |

| 1st party medical offered | Med Pay | Med Pay | Med Pay | PIP | Med Pay | Med Pay | PIP | MEB |

| Requirements | Optional | Optional | Optional | Guest PIP | Optional | Optional | Optional | Optional |

| Waiver needed? | No | No | No | Yes (to waive full PIP) | No | No | Yes | No |

| Statue of Limitations | 1 year | 3 years | 2 years | 3 years | 8 years | 3 years | 3 years | 3 years |

| Income loss included? | Not offered | Not offered | Not offered | Yes | Not offered | Not offered | Yes | Separate coverage |

PIP in TX and MD

PIP in TX and MD |

In addition to medical benefits and funeral expenses, personal injury protection (PIP) also includes loss of essential services benefits and loss of income benefits. Loss of essential services is designed to reimburse expenses accrued for services usually performed by the insured for the care and maintenance of the household while they are out on disability. This benefit would only be applicable to insureds not currently working at the time of the accident. Loss of income benefits is available to pay a percentage of the gross income lost by an insured while disabled from a vehicle accident (85% in MD; 80% in TX).

Guest vs. Full PIP in MD

In MD, the customer has the option to purchase either guest or full PIP. Full PIP would provide coverage for all insureds on the policy in addition to all passengers in the vehicle. Guest PIP, on the other hand, only provides coverage for guest passengers in the vehicle and any resident relative age 15 or younger. Guest PIP does not provide coverage for the insured, any drivers on the policy, or resident relatives age 16 or older.

Use this chart to understand the difference between how Full PIP and Guest PIP cover relatives:

If the customer chooses to carry only guest PIP, a waiver would need to be electronically signed within 7 days of the bind date, or full PIP will be added onto the policy.

PIP Unacceptable Risks

In Texas, there cannot be more than two PIP claims from the past 3 years across all rated drivers.

In Maryland, there cannot be more than one PIP claim from the past 3 years across all rated drivers.

Income Loss in VA

Income Loss in VA |

Separate from medical expense benefits, VA also offers income loss benefits. This coverage helps to reimburse the insured for income lost as a result of an injury from a vehicle accident. The limit for income loss is $100 a week multiplied by the number of vehicles on the policy up to a max of four vehicles. The statute of limitations on this coverage is one year from the date of the incident.